MARCH 2026 MARKET ANALYSIS FOR CHICAGO'S NORTH SIDE

Our monthly market analysis details six real estate metrics for the Near North Side, Lincoln Park, Lakeview and North Center, followed by our comprehensive monthly summary.

Please let us know if you need information on any of Chicago’s other neighborhoods

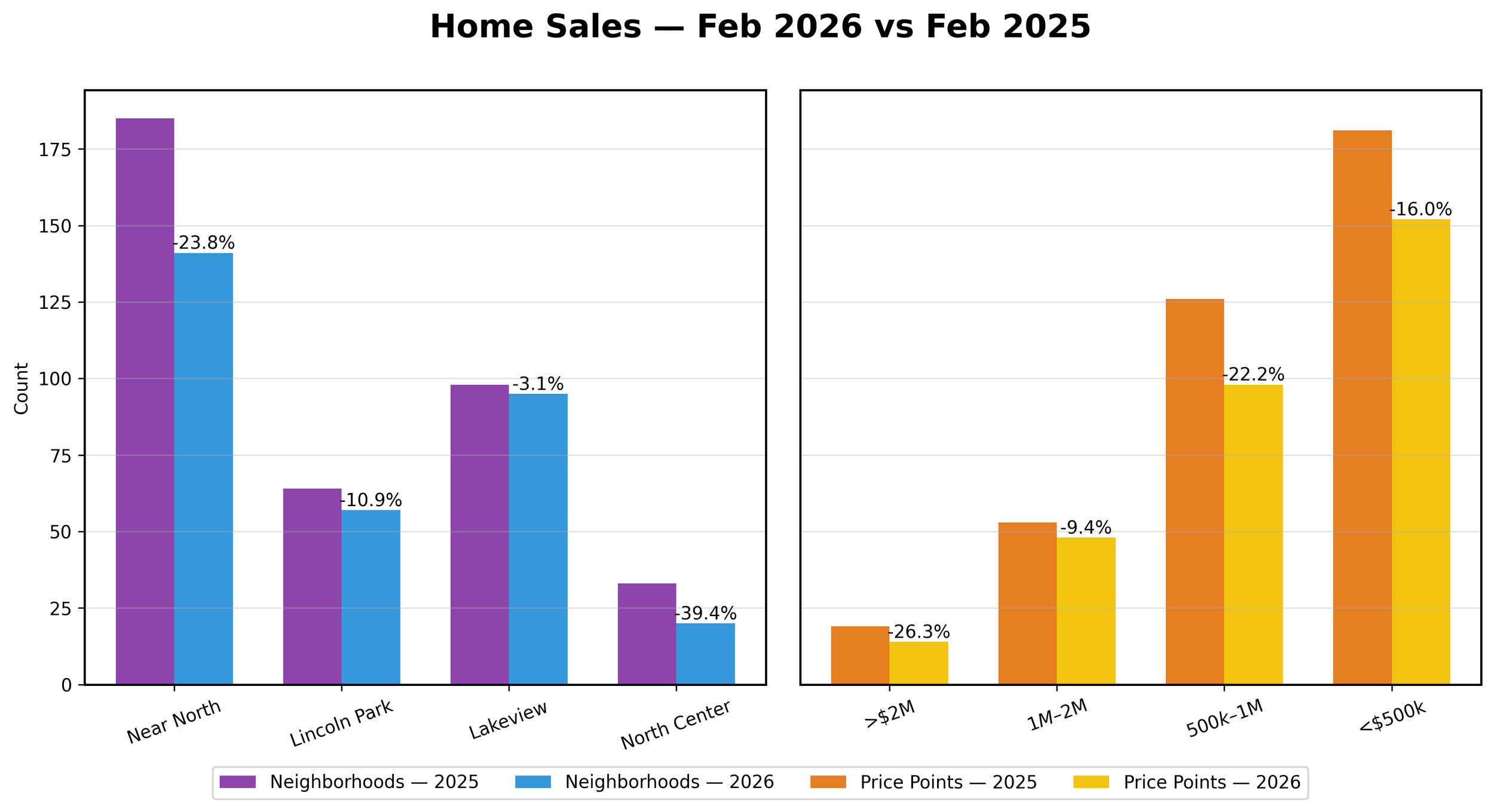

FEBRUARY HOME SALES

Year To Date 2026 vs 2025 - Down 19.9%

February 2026 vs 2025 - Down 17.6%

NOTEWORTHY:

Sales activity softened across nearly all segments, with the most pronounced slowdown in North Center and in the $500k–$1M price range.

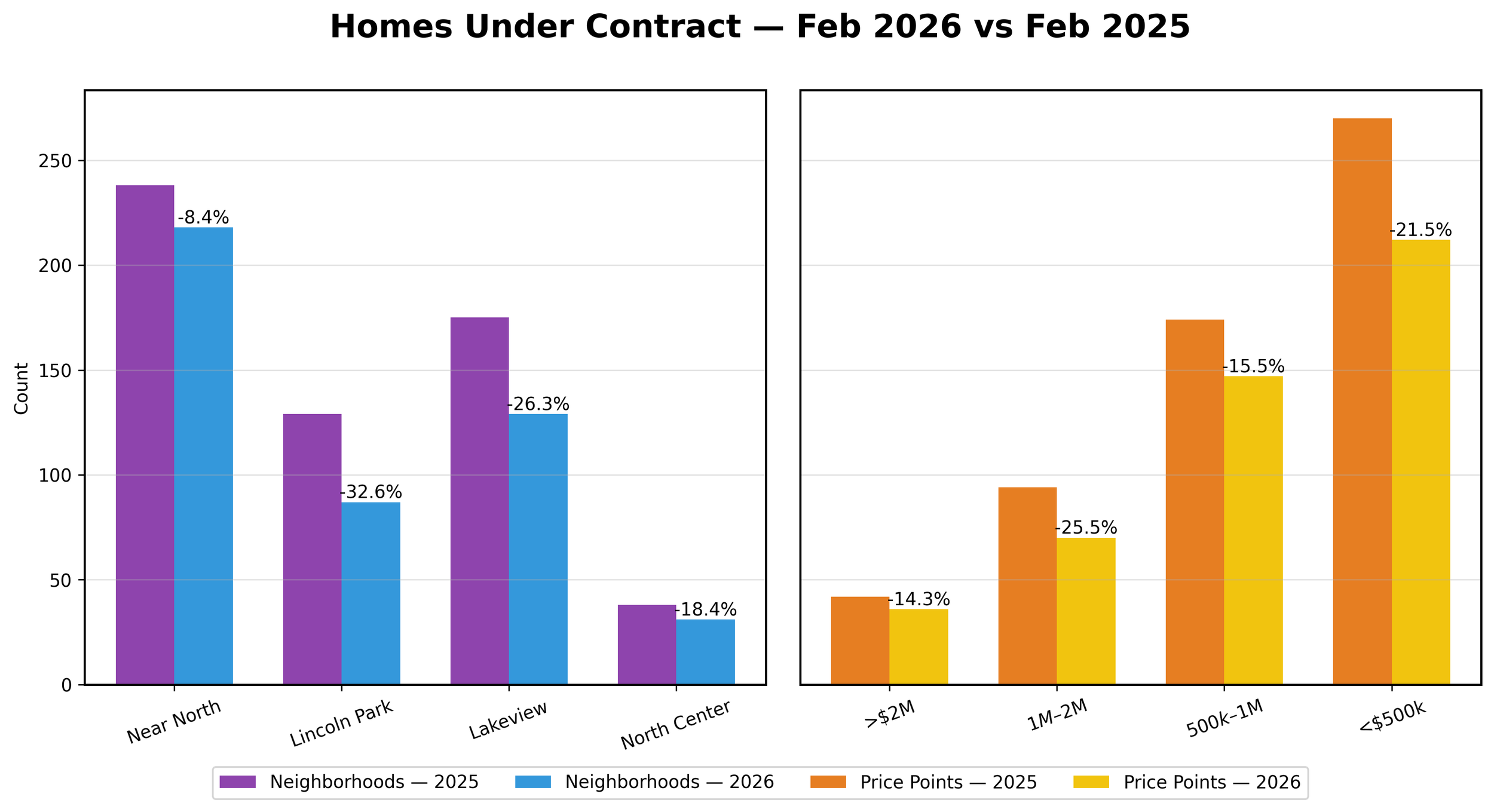

FEBRUARY HOMES UNDER CONTRACT

Year To Date 2026 vs 2025 - Down 19.8%

February 2026 vs 2025 - Down 19.8%

Noteworthy :

Most home sales that closed this month went under contract in a previous month. Units Under Contract reflects a more accurate picture of the current month, although not every home that goes under contract closes. February 2026 pending contracts declined across all segments, led by sharp drops in Lincoln Park and the $1M–$2M price band.

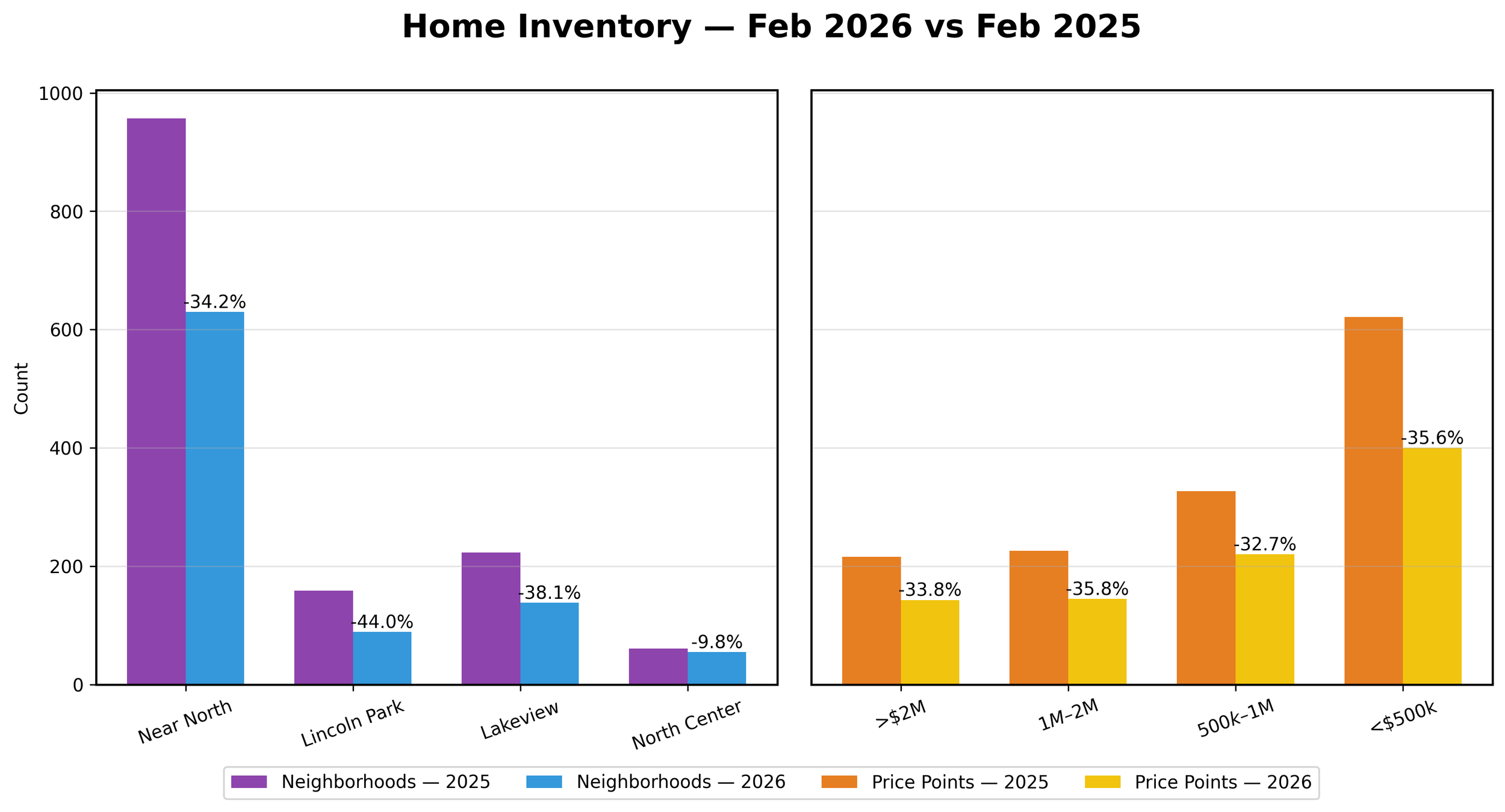

FEBRUARY HOMES FOR SALE

Year To Date 2026 vs 2025 - Down 33.5%

February 2026 vs 2025 - Down 33.5%

Noteworthy:

Inventory contracted sharply across nearly every segment, particularly in Lincoln Park and mid-market price tiers.

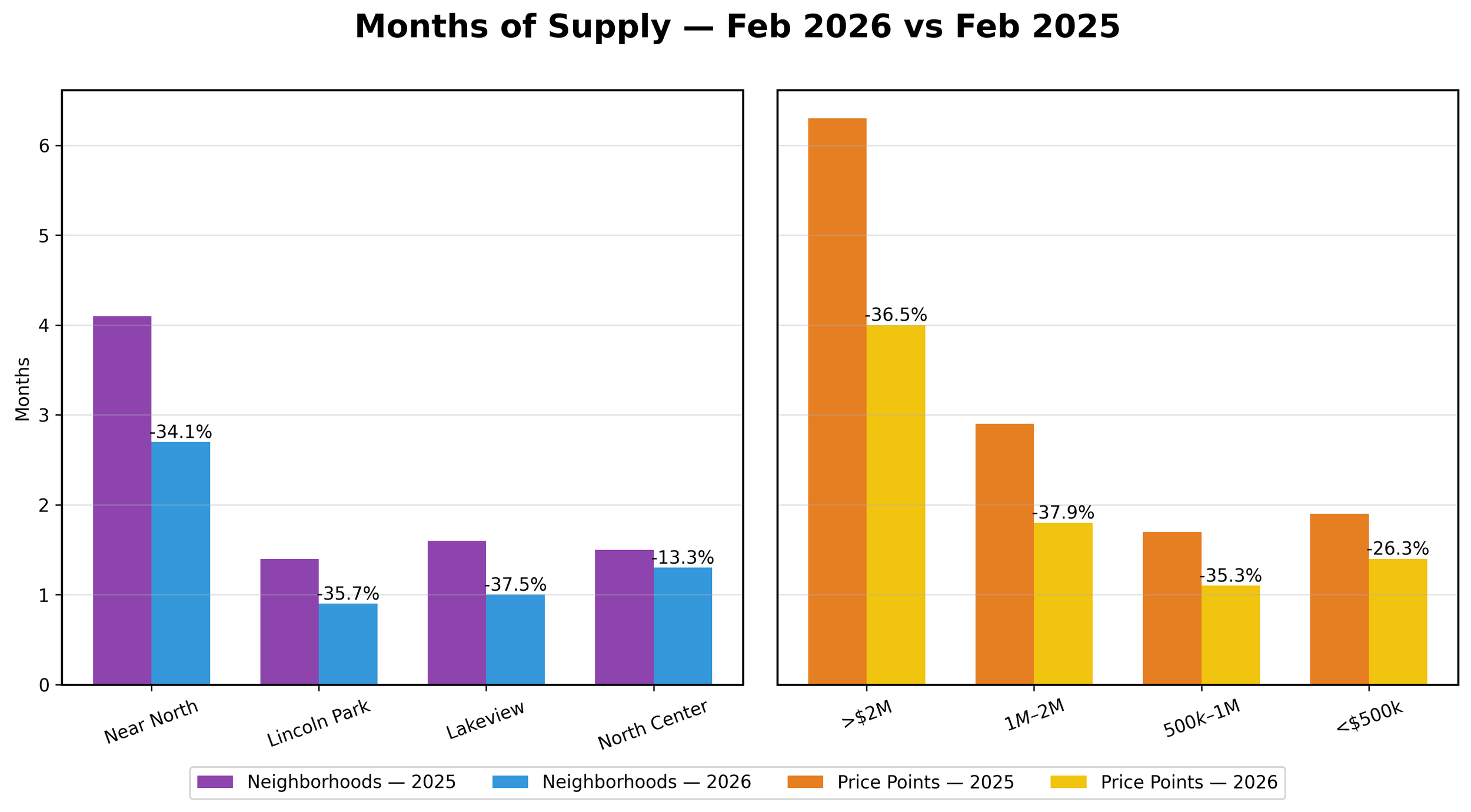

FEBRUARY MONTHS OF SUPPLY OF INVENTORY

Year To Date 2026 vs 2025 - Down 35.1% to 1.4 MSI

February 2026 vs 2025 - Down 35.1% to 1.5 MSI

Noteworthy :

Market supply tightened across the board, reinforcing a still-supply-constrained environment despite slower sales.

FEBRUARY MEDIAN PRICING

Year To Date 2026 vs 2025 - Up 1.6%%

February 2026 vs 2025 - Up 19.7%

Noteworthy :

Overall median pricing rose significantly, driven largely by strong gains in North Center and the luxury price tier.

FEBRUARY NEW LISTINGS

Year To Date 2026 vs 2025- Down 27.3%

February 2026 vs 2025 - Down 26.8%

Noteworthy :

Listing activity fell sharply, especially in Lincoln Park and mid-tier price ranges, further tightening supply conditions.

FEBRUARY SUMMARY

The February housing market showed moderating transaction activity alongside continued supply constraints, resulting in a mixed market environment where inventory remains tight despite slower sales and listing activity.

Market Activity

Closed sales declined compared to last year, reflecting softer seller activity across most neighborhoods and price segments. Total home sales fell approximately 18% year-over-year, with the most notable declines occurring in Near North and North Center. Lincoln Park and Lakeview experienced smaller drops, suggesting somewhat steadier demand in those neighborhoods.

Pending contracts also slowed, with homes under contract down roughly 20% from February 2025. The decline was most pronounced in Lincoln Park and Lakeview, indicating that buyer momentum, due to inventory constraints, has moderated across much of the market heading into the early spring season.

Supply Conditions

Inventory levels dropped sharply compared to last year, with the total number of homes on the market falling by more than one-third year-over-year. This decline was particularly significant in Lincoln Park and Lakeview, where available listings contracted the most.

As a result, months of supply also decreased, reinforcing that the market remains supply constrained despite slower transaction activity. Even with fewer buyers completing transactions, the reduced number of available homes continues to limit overall market balance.

Pricing Trends

Despite softer sales activity, median home prices increased overall, supported by limited inventory and continued demand for desirable properties. Price appreciation was especially strong in North Center, while Lakeview also saw notable gains. Lincoln Park experienced a modest decline in median price compared to the prior year.

Across price tiers, luxury properties above $2M saw the strongest price growth, while mid-market segments remained relatively stable.

New Listing Activity

New listing activity declined significantly compared to February 2025, with the number of homes entering the market falling by nearly 27% overall. Lincoln Park experienced the largest reduction in new listings, while North Center remained relatively stable.

Lower listing activity continues to be a key factor behind the persistent supply shortage seen across the market.

Overall Market Perspective

The February market reflects a supply-constrained environment with moderating demand. Transaction activity and pending contracts slowed year-over-year, yet inventory levels and new listings declined even more sharply. This imbalance has helped support home prices despite reduced sales volume.

As the spring market approaches, future market direction will likely depend on whether new listing activity increases enough to relieve the ongoing supply shortage.

Going Forward

With the current financial issues at the national and local levels, events continue to unfold. This makes it a challenge to predict with certainty how our local real estate will be affected. The single most positive aspect of this market is that there is an abundance of buyers who want to buy and live in our neighborhoods.

We will keep you updated.

YOUR HOME

A logical question would be “how does all of this affect the home that I am planning to sell or potentially buy?”

Every home is unique and a detailed analysis of your property and neighborhood is a necessity to fully understand the true market value and whether this is the right time to buy or sell.

There are many criteria both objective and subjective that must be analyzed in order to get a true picture.

Internet home pricing sites that claim to calculate your home’s value using only algorithms can be wildly inaccurate. Many market analysis from real estate agents that have not taken the time to personally tour the home can also be seriously flawed. Today’s volatility demands that you get a broker who thoroughly understands this rapidly changing market.

Whether you are buying or selling a home, we would welcome the opportunity to have a conversation about your real estate needs, goals and expectations.